Our California health insurance guide, including the FAQs below, is designed to help you understand the health coverage options and possible financial assistance available to you and your family. Having health coverage is especially necessary in California, as there’s a penalty on the state tax return for non-exempt filers who don’t have health coverage. 1

California runs its own state-run health insurance Marketplace/exchange, called Covered California. A dozen private health insurers offer coverage for individuals and families via Covered California. And California is one of the states where the exchange still offers a platform small businesses can use to purchase health coverage for their employees; four insurers offer small group plans through Covered California for 2024. 2

California is among the states where state-funded subsidies are available to Marketplace enrollees, in addition to federal subsidies. And California has allocated additional funding for the state subsidy program so that all Covered California enrollees will qualify for at least the Enhanced Silver 73 plan in 2025. 3 with lower out-of-pocket costs and no deductibles. 4

Under California rules, all of the plans sold in the exchange are standardized. 5 Standardized plans are available in most states. But although most states also have non-standardized plans available through the exchange, California does not. 6 This means that for certain services, all of the Covered California plans in a given metal level will have the same out-of-pocket costs.

A Covered California plan can be a great option if you need to buy your own health insurance. This includes people who aren’t eligible for Medicare or Medicaid, or don’t have an offer of affordable health insurance from an employer.

Hoping to improve your smile? Dental insurance may be a smart addition to your health coverage. Our guide explores dental coverage options in California.

Learn about California's Medicaid expansion, the state’s Medicaid enrollment and Medicaid eligibility.

Use our guide to learn about Medicare, Medicare Advantage, and Medigap coverage available in California as well as the state’s Medicare supplement (Medigap) regulations.

Short-term health plans provide temporary health insurance for consumers who may find themselves without comprehensive coverage. Learn more about short-term plan availability in California.

In order to sign up for private health coverage through Covered California, you must: 7

By those rules, most Californians can enroll in coverage through the exchange. But a bigger question for most people is financial assistance, and there are a few additional parameters to be eligible for subsidies through Covered California. To qualify for income-based Advance Premium Tax Credits (APTC), federal cost-sharing reductions (CSR), or California’s state-funded cost-sharing subsidies, you must:

Beyond those basic parameters, qualifying for Covered California subsidies will depend on how much your household earns. Here’s how household income is calculated under the ACA.

California AB570, enacted in October 2021, makes California the first state in the country to provide a pathway for some policyholders to add their parents to their health plan as dependents. 11

The legislation, which took effect in 2023, only applies to individual/family health plans (ie, not to plans that people get from an employer). Under the state law, a California resident with individual/family health coverage can cover parents as dependents, as long as the parents rely on the policyholder for at least 50% of their living expenses.

An earlier version of the bill would have applied to employer-sponsored health plans as well, but was opposed by business groups that worried about the cost. With the modification to make the legislation apply only to individual/family plans, the state expects that only about 15,000 people will use the option to add parents to their health plan. 12

California’s open enrollment period is longer than the window used in most other states. It begins November 1 and continues through January 31. 13 (In most states, open enrollment runs from November 1 through January 15.) And for 2024 coverage, an extension through February 9, 2024 was added at the last minute. 14

The open enrollment window is your opportunity to select a new plan or switch to a different plan. The enrollment window applies to plans obtained via Covered California or directly from an insurer, but note that subsidies are only available through Covered California.

For coverage to take effect on January 1, you need to complete your application by December 31. (This is later than the deadline in many other states.) If you enroll between January 1 and January 31, your coverage will take effect on February 1. 15 (For 2024 coverage, the extension of open enrollment through February 9, 2024 gave people an additional nine days to sign up with coverage backdated to February 1.) 14

After the annual open enrollment window ends, you may still be eligible to enroll or make a plan change if you experience a qualifying life event such as giving birth or losing other health coverage. And some people can enroll year-round even without a specific qualifying life event. 16

In addition to the standard list of qualifying events that trigger special enrollment periods nationwide, Covered California will also grant a special enrollment period to a person whose medical provider leaves their health plan’s network while the person is undergoing treatment for one of the following: 17

There is also a special enrollment period available if you have to pay the California penalty for not having health coverage the prior year. 17

In 2022, California enacted SB967, which creates an easy enrollment program in California as of the 2023 tax year (ie, for tax returns filed in early 2024). 18

Unlike most other states that have created or considered similar programs, the California legislation did not specifically create a special enrollment period for people deemed eligible for marketplace coverage (as opposed to Medicaid/CHIP, which is available year-round). However, Covered California does offer a special enrollment period specifically for people who have to pay a penalty on their state tax return for not having health insurance. A full list of Covered California’s special enrollment opportunities is available here.

Enrollment in Medi-Cal (California Medicaid) is available year-round.

To enroll in an ACA Marketplace/exchange plan in California, you can:

The Affordable Care Act (ACA) provides income-based subsidies that can reduce the amount you pay for your coverage each month. In California, these subsidies are available to applicants who meet the eligibility requirements and enroll in a health plan through Covered California.

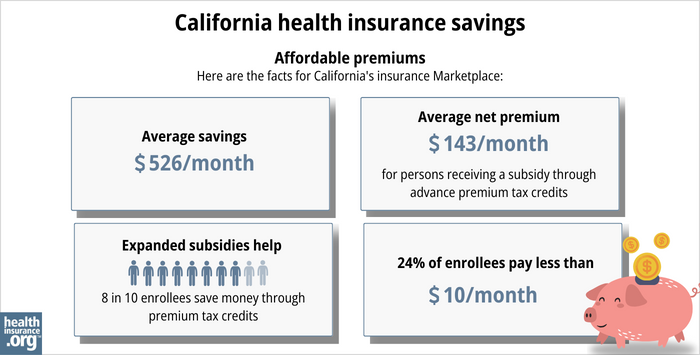

Nearly nine out of ten Covered California enrollees were receiving premium subsidies as of early 2024. These subsidies averaged about $523/month, and after the subsidies were applied, the average enrollee’s premium was about $186/month. 20

If your household income isn’t more than 250% of the federal poverty level, you’ll also be eligible for federal cost-sharing reductions (CSR), which will reduce your deductible and other out-of-pocket expenses. These benefits are built into Silver-level plans if the applicant is eligible for them. Forty-four percent of Covered California enrollees were receiving CSR benefits as of 2024. 21

And as of 2024, California is supplementing the federal CSR benefits with additional state-funded cost-sharing subsidies. Eligible Silver-plan enrollees have $0 deductibles and lower costs for other out-of-pocket expenses. 22

California has allocated additional funding to the state subsidy program for 2025. This will ensure that all Covered California enrollees will qualify for at least the Enhanced Silver 73 plan, 3 which offers reduced out-of-pocket costs and no deductibles. 4

Covered California and Medi-Cal (California Medicaid) use the same application, and the system will let you know whether you’re eligible for Medi-Cal or a private plan through Covered California – with subsidies if you qualify for them.

California does not allow short-term health insurance policies to be sold, under the terms of legislation that the state enacted in 2018. 24

For 2024 coverage, 12 insurers offer plans through California’s exchange. This is the same as the number of participating insurers in 2023, but there was one insurer exit at the end of 2023 and one newcomer for 2024. (Oscar Health Plan of California left at the end of 2023, while Inland Empire Health Plan is new for 2024.) 25

All 12 carriers have filed rates and plans for 2025, so carrier participation is expected to remain unchanged. 4

Covered California’s insurers have proposed the following average rate changes for 2025, which amount to an overall average rate increase of 7.9%: 4 These rates are under review by state regulators and will be finalized before open enrollment begins in November 2024.

Source: Covered California 4

It’s important to remember that average rate changes are for full-price plans (i.e. before any subsidies are applied), and most enrollees do not pay full price: Nearly nine out of ten of Covered California enrollees were receiving premium subsidies in 2023, to offset some or all of their monthly payments. 26

The subsidy amount is different for each enrollee and changes each year depending on the cost of the second-lowest-cost Silver plan relative to the enrollee’s household income. Under the American Rescue Plan and the Inflation Reduction Act, subsidies are larger and more widely available than they used to be, and that will continue to be true at least through 2025.

Full-price (unsubsidized) premium changes depend on the specific plan (for each insurer, premium changes vary from one plan to another), as well as the enrollee’s age and zip code.

So, for the majority of Covered California enrollees, net premium changes will depend on how their specific plan’s rate changes, as well as year-over-year changes in their subsidy amount.

If the cost of your current plan is increasing for the coming year, you may want to consider some of the other plans that are available via Covered California. You might find some that are less expensive and offer similar benefits.

Here’s a look at how average full-price (pre-subsidy) premiums have changed over the years in California’s individual/family market:

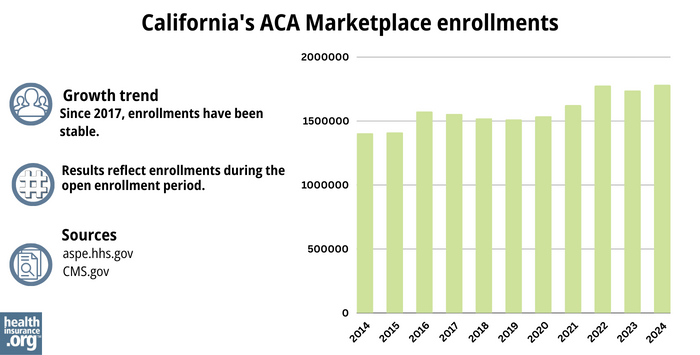

CMS reported that 1,784,653 people enrolled in 2024 plans through Covered California during open enrollment. 37

Here’s a summary of historical enrollment numbers for Covered California:

Source: 2014, 38 2015, 39 2016, 40 2017, 41 2018, 42 2019, 43 2020, 44 2021, 45 2022, 46 2023, 47 2024 48

Covered California: This is California’s Marketplace/exchange. Residents can use Covered California to enroll in individual/family health plans and receive income-based subsidies, and also to enroll in Medi-Cal. You can contact Covered California at 800-300-1506.

California Department of Managed Health Care (DMHC): Regulates the vast majority of California’s commercial (non-self-insured) health plans, and assists consumers and businesses with insurance-related questions and concerns.

California Department of Insurance: Regulates California’s insurance plans that aren’t regulated by the DMHC. If a complaint or concern is filed with the DMHC and it’s for a product that’s regulated by the Department of Insurance, it will be forwarded to the Department of Insurance.

California Health Insurance Counseling and Advocacy Program (HICAP): A service for California Medicare beneficiaries and their caregivers. HICAP provides information and assistance with questions related to Medicare eligibility, enrollment, and claims.

Louise Norris is an individual health insurance broker who has been writing about health insurance and health reform since 2006. She has written dozens of opinions and educational pieces about the Affordable Care Act for healthinsurance.org.